How a federal indictment in Massachusetts exposes the fastest-growing identity scheme in rental housing – and what it tells operators about the next thousand applications in their pipeline.

What Is Synthetic Identity Fraud in Rental Housing?

Synthetic identity fraud in multifamily housing occurs when someone uses a stolen Social Security number – often belonging to a child, senior citizen, or incarcerated person – combined with fabricated income documents and rented credit tradelines to create a fraudulent applicant profile. The resulting application clears standard screening checks because the credit score is real for that number. The paystub and bank statement match. But neither the identity nor the income belongs to the person signing the lease.

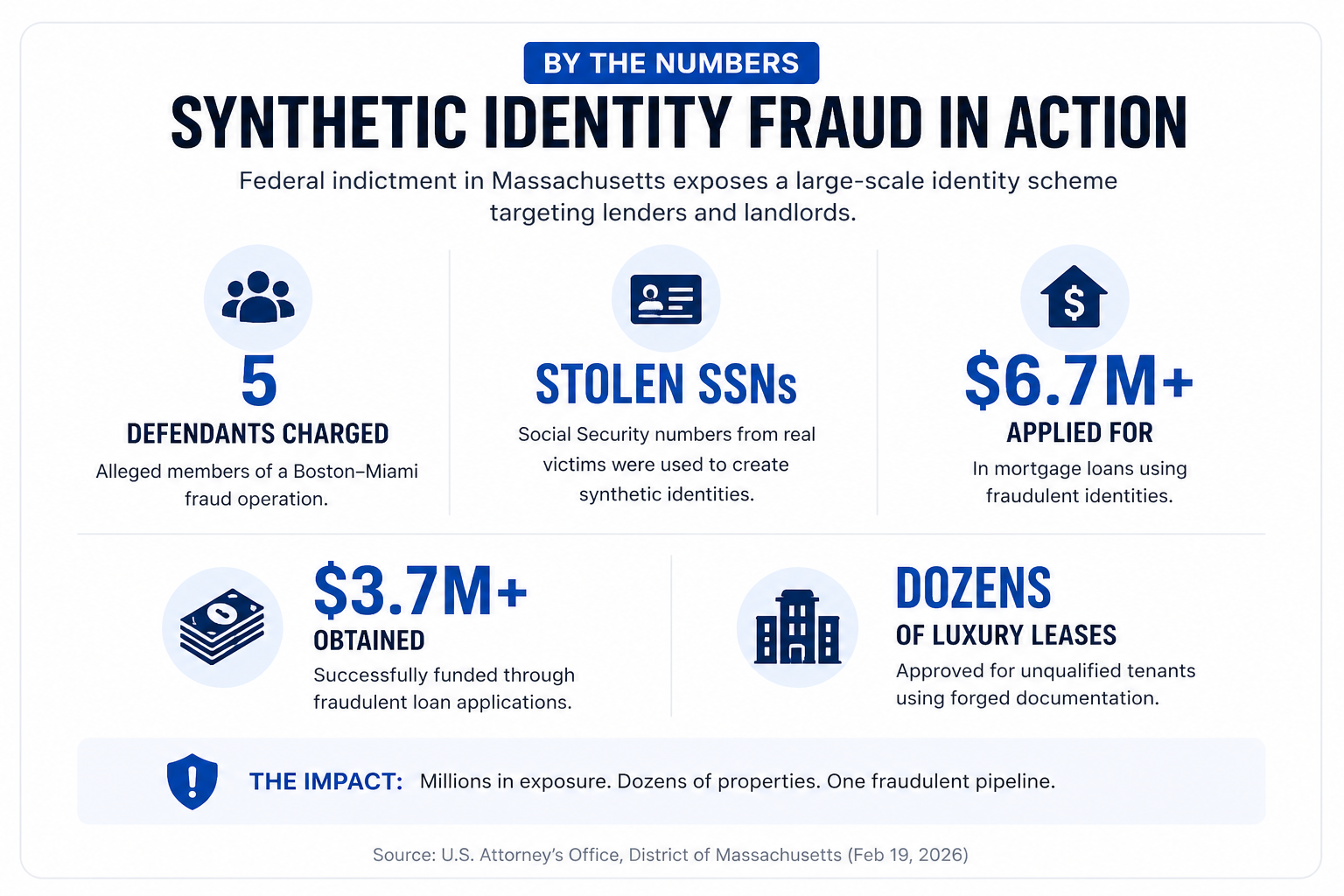

On February 19, 2026, the U.S. Attorney for the District of Massachusetts indicted five defendants for running exactly this scheme – generating over $6.7 million in fraudulent mortgage and rental applications, securing more than $3.7 million, and placing unqualified tenants in dozens of luxury apartments. Stopping this requires three things standard screening cannot do: verify the SSN directly against the Social Security Administration, authenticate document metadata rather than just its appearance, and independently recalculate income from source data.

Key Takeaways

- 5 defendants charged in a 2026 Massachusetts federal indictment; $3.7M+ obtained through the scheme

- Stolen SSNs most often come from children, seniors, incarcerated individuals, and recent immigrants

- Standard credit screening cannot detect CPN-based synthetic identities – the score is real for that number

- Document authentication requires metadata analysis; visual review cannot catch modern forgeries

- Docuverus detects synthetic identity fraud with 99.98% accuracy across multifamily portfolios

Fraud is not a one-off problem anymore. It is a pipeline. And on February 19, 2026, the U.S. Attorney for the District of Massachusetts gave the multifamily industry one of the cleanest looks at that pipeline we have seen in years.

Five defendants. Stolen Social Security numbers. Borrowed credit profiles. Forged paystubs. Doctored bank statements. Over $6.7 million applied for in mortgage loans. More than $3.7 million obtained. And dozens of luxury apartment leases handed over to people who never should have been approved.

Source: U.S. Attorney’s Office, District of Massachusetts (Feb. 19, 2026).

This is Fraud Spotlight #1 – a recurring breakdown of real cases working their way through federal courts and the lessons multifamily operators need to take from each one. We are starting here because this case is the textbook version of the fraud that is hitting your screening queue right now: SSN and CPN fraud.

What the 2026 Massachusetts Indictment Revealed

According to the U.S. Attorney’s Office, the alleged ringleader ran what looked like a tax preparation and credit repair shop with offices in Boston and Miami. Behind the storefront, prosecutors say, the operation manufactured the documentation needed to push unqualified applicants past lender and landlord checks.

The mechanics, as alleged in the charging documents:

- Stolen Social Security numbers from real victims were funneled in by a co-defendant and handed to applicants to use on mortgage and lease applications.

- Tradelines – authorized-user spots on strangers’ high-limit, long-history credit accounts – were attached to those applicants to inflate credit scores overnight.

- Fake paystubs were paired with altered bank statements showing balances and deposits engineered to match. The numbers were not random. They were tuned to the income the application claimed.

- Identity layering – one defendant allegedly let her name and ID be used to sign leases on behalf of the real, unqualified tenants, hiding who was actually moving in.

The defendants are presumed innocent until proven guilty. But the playbook described in the indictment is not new, and it is not isolated. It is the same one being sold on social media in $300 packages right now.

What Is a CPN and Why Does It Pass Standard Screening?

If you have heard the term CPN floating around credit repair forums, this is where it lives. A Credit Privacy Number – sometimes marketed as a Credit Profile Number – is a nine-digit number sold as a “second-chance SSN.”

It is not a legal product. In nearly every case, a CPN is a real SSN that has been quietly lifted from someone who is unlikely to notice quickly: a child, a senior, an incarcerated person, or a recent immigrant. When an applicant types one into your rental form, you are not seeing a clean credit profile. You are seeing identity theft in real time.

Pair that CPN with a rented tradeline, a polished paystub, and a bank statement that has been retouched in the right places, and the file looks pristine on the surface. Credit score? Strong. Income-to-rent ratio? Comfortable. Bank balance? More than enough. Underneath it, none of it belongs to the person signing the lease.

Why Multifamily Is the Primary Target for Synthetic Identity Fraud

The Massachusetts case names mortgage lenders and landlords in the same breath for a reason. The same forged-document kit clears both. And rental applications, by design, are the lower-friction target.

Three structural realities make multifamily the soft entry point:

- Speed pressure. Vacancy loss compounds daily. Leasing teams are graded on how fast they close, not how deep they dig.

- PDF-and-screenshot workflows. Most screening still relies on uploaded documents that are trivially easy to alter and visually impossible to vet at scale.

- Surface-level credit checks. A bureau pull confirms a number exists and a score is attached. It does not confirm the applicant is the human that number was issued to.

That is the gap the alleged Boston-Miami operation drove a truck through. And it is the gap the next operation, and the one after that, will keep driving through until verification catches up to the threat.

Three Steps That Stop Synthetic Identity Fraud

Three shifts separate the portfolios that absorb this fraud from the ones that catch it:

- Verify the identity, not just the score. Confirm the SSN traces to the actual applicant – not a lifted number attached to a synthetic file.

- Read the document, not the image. Paystubs and bank statements carry metadata, edit histories, and structural fingerprints. A real verification engine reads those layers. A human eyeball cannot.

- Recompute the income. Stop accepting the number on the paystub at face value. Recalculate from source data and flag anything that does not reconcile.

How Docuverus Detects Synthetic Identity Fraud

Docuverus is the only verification platform that solves all three at once. Our document-first platform combines Multidimensional Metadata Analysis, identity validation, and full income recalculation – so the file you approve is the file you actually have, not the one a fraud kit assembled for you.

We catch the altered bank statement. We catch the borrowed tradeline pattern. We catch the SSN that does not match the human typing it. And we calculate the real income behind the paystub instead of trusting the printed number.

The Massachusetts indictment is one case. The pipeline behind it is feeding thousands of applications into multifamily portfolios every week. The operators who win this cycle are the ones who stop screening like it is 2019.

Fraud has gone industrial. Verification has to match it.

Frequently Asked Questions

What is synthetic identity fraud in rental housing?

Synthetic identity fraud in rental housing occurs when an applicant uses a stolen Social Security number combined with forged income documents and rented credit tradelines to appear qualified. The resulting credit profile passes standard screening because the score is real – but it belongs to a different person.

What is a CPN (Credit Privacy Number)?

A CPN is a nine-digit number sold as a “second-chance SSN.” In nearly every case it is a stolen SSN taken from someone unlikely to notice – a child, senior citizen, incarcerated person, or recent immigrant. Using a CPN on a housing application constitutes identity fraud under federal law.

Why does standard credit screening fail to detect CPN-based fraud?

Standard credit pulls confirm that a number exists and has a score attached. They do not confirm the human presenting the number is its legitimate owner. CPN fraud exploits this gap – the score is real for that number; the fraudster simply is not the person it was issued to.

How do property managers detect synthetic identity fraud?

Stopping synthetic identity fraud requires three steps: verify the SSN directly with the Social Security Administration (not just a bureau pull), authenticate income document metadata rather than just visual appearance, and independently recalculate income from source data.

What did the 2026 Massachusetts indictment reveal about rental fraud?

A February 2026 federal indictment charged five defendants with running a scheme that used stolen SSNs, rented credit tradelines, forged paystubs, and doctored bank statements to obtain over $3.7 million in fraudulent loans and dozens of luxury apartment leases.

Sources

U.S. Department of Justice, District of Massachusetts – Five Individuals Charged with Multi-Million Dollar Mortgage and Apartment Fraud Scheme (Feb. 19, 2026)